The PEA, completed by G Mining Services Inc. (“GMS“) as lead consultant, supported by other engineering consultants, confirms robust economics for a low-cost, large-scale, conventional open pit (“OP“) and underground (“UG“) mining and milling operation, with operating costs below industry averages, in addition to a high rate of return. The Project is ideally sequenced to leverage the strong macroeconomic conditions including a strong gold (“Au“) price, lower inflation, and Guyana’s rapidly developing economy.

Louis-Pierre Gignac, President & Chief Executive Officer, commented: “The Oko PEA, based on the long-term consensus gold price of $1,950 per ounce, outlines a high-production, long-life, high-margin operation with an after-tax NPV5% of $1.4 billion and IRR of 21%. Oko is ideally sequenced to benefit from GMIN’s regional footprint, development expertise, anticipated free cashflow from our in-production Tocantinzinho Gold Mine in Brazil and historically high gold prices. GMIN announced last week commercial production at Tocantinzinho, delivering our first operating mine on-time and on-budget, and we will seek to repeat this success with Oko using essentially the same team. I am excited that this exceptionally positive PEA only captures a snapshot of the potential value of Oko, as we continue to explore the prospective land package and evaluate value-enhancement opportunities for improved economics in a feasibility study planned for the first quarter of 2025. I look forward to the tremendous shared-value creation for our stakeholders, including the country of Guyana.”

PEA Overview

Oko is planned as a mix of conventional OP mine and mechanized long hole open stoping UG mine, with on-site treatment of the mined material processed through a conventional circuit consisting of comminution, gravity concentration, cyanide leach and adsorption via carbon-in-leach (“CIL“), carbon elution and gold recovery circuits. The OP mine will have a Life of Mine (“LOM“) of 15 years, including 2 years of pre-stripping, from 4 pit phases, while the UG mine will have a LOM of 13 years, including 2 years of development, in 3 zones. The mill will operate for 13 years.

The PEA is derived using the Corporation’s mineral resource estimate effective as at February 7, 2024 (the “MRE“). The effective date of the PEA is September 4, 2024, and a NI 43-101 compliant technical report (the “Technical Report“) will be filed on the Corporation’s website and under its SEDAR+ profile within 45 days of this news release.

Table 1: Oko West Preliminary Economic Assessment Highlights

Description

Units

Figure

Production Data

OP Mill Feed Tonnage

Mt

61

UG Mill Feed Tonnage

Mt

15

Total Mineralized Material Mined

Mt

75

Total Waste Mined (OP and UG)

Mt

367

Total Tonnage Mined (OP and UG)

Mt

443

Strip Ratio

waste : mineralized material

6.0

Average Milling Throughput

Mt/year

6.0

Average Milling Throughput

tpd

16,110

Gold Head Grade

g/t

2.00

OP Head Grade

g/t

1.72

UG Head Grade

g/t

3.19

Contained Gold

koz

4,848

Average Recovery

%

92.8 %

Total Gold Production

koz

4,500

Mine Life

years

12.7

Average Annual Gold Production

oz

353,000

Operating Costs (Average LOM)

Total Site Costs

USD/oz

$728

Government Royalties

USD/oz

$126

Total Operating Cost

USD/oz

$853

AISC

USD/oz

$986

Capital Costs

Total Upfront Capital Cost

USD MM

$936

Initial UG Capital Costs (Sustaining Capital)

USD MM

$124

OP and UG Sustaining Capital

USD MM

$413

Life of Mine Sustaining Capital

USD MM

$537

Closure Costs

USD MM

$37

Total Capital Costs

USD MM

$1,510

Financial Evaluation

Gold Price Assumption

USD/oz

$1,950

After-Tax NPV 5%

USD MM

$1,367

After-Tax IRR

%

21 %

Payback

Years

3.8

Table 2: Sensitivity Analysis

Downside

Base

Spot

Scenario

Case

Case

Case

Gold Price

USD/oz

USD MM

$1,600

$1,950

$2,500

After Tax NPV5%

$639

$1,367

$2,502

Payback

Years

5.9 Years

3.8 Years

2.0 Years

After-Tax IRR

%

13 %

21 %

31 %

Average Annual EBITDA

USD MM

$264

$376

$554

Average Annual Free Cash Flow

USD MM

$188

$272

$406

LOM EBITDA

USD MM

$3,452

$4,924

$7,238

LOM Free Cash Flow

USD MM

$1,475

$2,584

$4,325

Note: Average annual figures represent the 12.7-year operating period.

Table 3: Sensitivity Analysis cont’d

After Tax

Average Annual

Gold Price

NPV5%

IRR

Payback

EBITDA

FCF

(USD/oz)

(USD M)

( %)

(years)

(USD M)

(USD M)

$1,300

($4)

5 %

10.4

$167

$115

$1,400

$214

8 %

8.3

$199

$139

$1,500

$427

10 %

6.9

$231

$163

$1,600

$639

13 %

5.9

$264

$188

$1,700

$849

15 %

5.2

$296

$212

$1,800

$1,057

18 %

4.5

$328

$236

$1,900

$1,264

20 %

4.0

$360

$260

$1,950

$1,367

21 %

3.8

$376

$272

$2,000

$1,471

22 %

3.6

$392

$285

$2,100

$1,677

24 %

3.3

$425

$309

$2,200

$1,883

26 %

3.0

$457

$333

$2,300

$2,090

27 %

2.0

$489

$357

$2,400

$2,296

29 %

2.0

$521

$382

$2,500

$2,502

31 %

2.0

$554

$406

$2,600

$2,708

33 %

2.0

$586

$430

Note: Average annual figures represent the 12.7-year operating period.

Property Description, Location and Access

Oko is an advanced-stage gold development project, which straddles the Cuyuni-Mazaruni Mining Districts (administrative Region 7) in north central Guyana, South America. The Project is located approximately 100 kilometres (“km”) southwest of Georgetown, the capital city of Guyana and approximately 70 km from Bartica, the capital city of Region 7 (Figure 2). The Project comprises one Prospecting Licence (“PL”) issued to Reunion Gold Inc., GMIN’s indirect 100%-owned Guyanese subsidiary, on September 23, 2022. The PL is valid for three years and is renewable for up to two years. The PL has a surface area of approximately 10,890 acres (4,407 hectares).

In March 2024, an option agreement was entered into for the Northwest extension mining permits, consisting of three medium-scale mining permits (“MPMS”) adjacent to the PL. That agreement is valid for five years with a possible two-year extension. In August 2024, another agreement was concluded to purchase additional MPMS from a private group of individuals for the Eastern and Southern extensions to the PL.

The Project can be accessed via numerous methods: helicopter direct from Ogle airport to the site, fixed-wing plane from Ogle airport to Bartica airstrip, or by car and then speedboat. From the town of Itabali at the confluence of the Cuyuni and Mazaruni rivers, one can use the Puruni or the Aremu laterite roads, using four-wheel drive vehicles. Bartica is accessible by a 20-minute direct flight from the Ogle airport in Georgetown or by road and boat from Parika on the Essequibo River. There are regular boat services between Bartica and Parika.

The climate is equatorial and humid. The Project has operated throughout the year without any interruptions related to the weather.

Mineral Resource Estimate

Measured and Indicated Mineral Resources (“M&I”) total 64.6 million tonnes (“Mt”) at an average gold grade of 2.05 grams per tonne (“g/t Au”) for 4.27 million contained ounces of gold. Contained gold in the M&I category represents 73% of the global resource.

The MRE considers 397 diamond drill holes, 292 reverse circulation holes, and 59 trenches completed by Reunion Gold Corporation between December 2020 and January 2024.

Table 4: Mineral Resource Estimate

Category

Tonnes

(kt)

Gold Grade

(g/t)

Contained Gold

(koz)

Pit Constrained Resource

Indicated

64,115

2.06

4,237

Inferred

8,107

1.87

488

UG Constrained Resource

Indicated

491

1.85

29

Inferred

11,510

3.01

1,116

Total OP and UG

Indicated

64,606

2.05

4,266

Inferred

19,617

2.54

1,603

These Mineral Resources are not Mineral Reserves as they have not demonstrated economic viability. All figures are rounded to reflect the relative accuracy of the estimates. The lower cut-offs used to report open pit Mineral Resources are 0.30 g/t Au in saprolite and alluvium/colluvium, 0.313 g/t Au in transition, and 0.37 g/t Au in fresh rock. Underground Mineral Resources are reported inside potentially mineable volume and include below cut-off material (stope optimization cut-off grade of 1.38 g/t Au). A change in the reporting method for the underground part of the deposit explains the differences in tonnage and average grade between this PEA and the MRE published in February 2024. Tonnage of potentially mineable material stated below cut-off (i.e., must take material) is declared for this constrained underground Mineral Resource Estimate. Blocks have been reclassified inside each stope based on deposit knowledge and continuity and reflect the existing classification. No changes in total ounces is observed. The cut-off grades are based on a gold price of US$1,950 per troy ounce and show 96.0%, 95.0% and 92.5% processing recoveries for saprolite and alluvium/colluvium, transition and fresh rock, respectively.

Production Profile

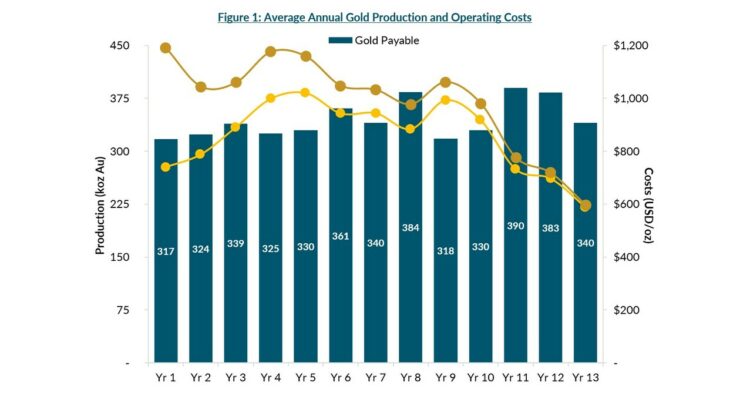

The PEA outlines an average annual gold production profile of 353 thousand ounces (“koz”) over the 12.7-year mine life. Total gold production is 4.5 million ounces with an average gold grade milled of 2.00 g/t Au, and metallurgical recovery of 92.8%.

The processing feed will be supplied by the open pit during the initial three years of commercial production. Starting in the fourth year of production, underground mining will contribute a significant tonnage of mineralized material.

Table 5: Gold Production by Mil Feed Type

Open Pit

Underground

Total OP + UG

Material

Grade

Contained

Material

Grade

Contained

Contained

Gold

Milled

Milled

Gold

Milled

Milled

Gold

Gold

Recovery

Recovered

Year

(kt)

(g/t)

(koz)

(kt)

(g/t)

(koz)

(koz)

( %)

(koz)

Year 1

6,368

1.63

334

40

1.97

3

336

94 %

317

Year 2

6,933

1.54

343

67

2.09

4

348

93 %

324

Year 3

6,714

1.58

340

286

2.63

24

365

93 %

339

Year 4

6,054

1.41

275

946

2.39

73

347

94 %

325

Year 5

4,655

1.46

219

1,345

3.18

138

357

93 %

330

Year 6

4,405

1.51

213

1,595

3.43

176

389

93 %

361

Year 7

4,432

1.46

208

1,568

3.16

159

368

93 %

340

Year 8

4,260

1.86

255

1,562

3.19

160

416

93 %

385

Year 9

3,455

1.72

192

1,545

3.08

153

344

93 %

319

Year 10

3,489

1.90

213

1,511

2.96

144

357

93 %

331

Year 11

3,518

2.31

261

1,482

3.37

161

422

93 %

390

Year 12

3,572

2.23

256

1,428

3.45

158

415

93 %

384

Year 13

2,406

3.04

235

1,125

3.66

132

367

93 %

340

Total

60,261

1.72

3,345

14,501

3.19

1,485

4,831

93 %

4,484

Mining

The Project is planned as a mining operation that integrates both conventional open pit mining and mechanized long hole open stoping for the underground mine.

The main OP is centered on Block 4 with two smaller sub-pits positioned on the northern and southern extensions to the main pit. A total of 60.7 Mt of mineralized material will be mined from the OP at an average diluted gold grade of 1.72 g/t Au. 0.4 Mt of this material will be milled during the pre-production period. A total of 364.6 Mt of combined waste and overburden will be extracted, resulting in a strip ratio of 6.0x. The OP operation will be executed in 4 phases over 15 years, including 2 years of pre-production, with an owner-operated mining fleet.

The UG operation will take place in three zones: the main zone and two satellite zones, all accessible from a surface mine portal through the same main decline ramp. Long hole open stoping mining method will be used, including transverse stoping and longitudinal stoping variations. The average UG production rate is expected to be 4,250 tonnes per day (“tpd“) of mineralized material, with 4,000 tpd and 250 tpd from stope production and lateral development, respectively. A total of 14.5 Mt of mineralized material is expected to be mined at an average diluted gold grade of 3.19 g/t Au. The UG mine is expected to be in production for 13 years, including a two-year development period. The initial 2 years of construction and development will use contract mining and transition to owner-operated mining thereafter.

Processing and Recovery

The proposed process plant design for Oko is based on a standard metallurgical flowsheet to treat gold bearing material and produce doré. The process plant is designed to nominally treat 6.0 Mtpy of fresh rock and will consist of comminution, gravity concentration, cyanide leach and adsorption via carbon-in-leach (“CIL“), carbon elution and gold recovery circuits. CIL tailings will be treated in a cyanide destruction circuit and pumped to a tailings storage facility.

The milling rate is initially set at 6.0 million tonnes per annum (“Mtpa“) for hard rock but will be increased to 7.0 Mtpa when saprolite and transition materials are added. During the open pit operational period, the ramp-up period is 5 months. The mill will operate for 13 years.

Select key design criteria include crushing plant availability of 70%; grinding, gravity, CIL, gold recovery and tailings handling circuit availability of 92% through the use of standby equipment in critical areas, inline crushed material stockpile and reliable power supply; comminution circuit to produce a primary grind size of (P80) 80% passing 75 µm; and CIL residence time of 48 hours to achieve optimal gold extraction.

Table 6: Metallurgical Recoveries

Feed

Total

Mill

Feed Material

Grade

Recovery

Feed

Saprolite

1.40

96 %

10 %

Transition

1.47

95 %

5 %

Fresh Rock

2.11

93 %

85 %

Total LOM

2.00

93 %

100 %

Power

Plant site activities, including the process plant, UG mining, OP mine, and balance of plant infrastructure, will require an average of 37 megawatts (“MW“) at full operation. The plant’s full power consumption was benchmarked against similar projects, with OP mining and UG mining adjusted for processing throughputs.

The Project’s base case scenario considers installing a dedicated Heavy Fuel Oil (“HFO“) fired power plant. The power plant is anticipated to comprise six 9.4 MW engine generating sets (“genset“), totaling 56.4 MW installed capacity and 42.3 MW running capacity. This assumes that one of the generators would be on standby. One additional genset is planned in sustaining capital to allow for maintenance activities.

Alternative power supplies will be studied as part of the Feasibility Study, including using liquefied natural gas (“LNG”) power plant.

Environmental and Permitting

Between 2022 and 2024, comprehensive physical, biological, and social baseline studies were conducted to support Project planning, including environmental assessments during both dry and wet seasons. These studies aim to identify potential concerns and recommend actions for effective Project design and regulatory compliance. The Project area is not a priority conservation site and does not overlap with any protected or Indigenous lands. Ongoing data collection will help refine Project design, identify potential environmental and social impacts, and contribute to the submission of an Environmental Impact Assessment (“EIA“). Future studies will also address additional project components such as power supply and road access.

The permitting process for the Oko involves obtaining environmental authorization from Guyana’s Environmental Protection Agency (“EPA“) following the submission and approval of an EIA, which GMIN expects to file by year end 2024. Exploration activities are conducted under a previously received no-objection letter from the EPA.

The necessary permits covering the construction of the mine, processing plant, transmission line, port, HFO power generation, and access road, will be issued after the EPA’s review, which GMIN anticipates may take approximately six months after submission of the EIA. GMIN’s permitting activities will be guided by ongoing stakeholder engagement and government consultations, ensuring compliance with environmental and social international standards.

Operating Costs

LOM operating costs are estimated at $728 per ounce of gold produced, excluding royalty costs, as summarized below. The LOM AISC is estimated to be $986 per ounce of gold produced based on average annual gold production of 353,000 ounces over the 12.7 years of mine life. The cost structure places the Project in the bottom quartile of the global gold cost curve.

Table 7: Operating Cost and AISC Summary

Costs

Unit Cost

Unit Cost

(USD/t milled)

(USD/oz)

Mining Costs – OP

$13.13

$219

Mining Costs – UG

$10.76

$179

Rehandle Costs

$0.15

$2

Processing Costs

$9.04

$151

Power Costs

$5.93

$99

G&A Costs

$4.14

$69

Transport & Refining

$0.48

$8

Total Site Cost

$43.62

$728

Royalty Costs

$7.53

$126

Total Operating Costs

$51.15

$853

Sustaining Capex

$7.19

$120

Closure Costs

$0.49

$8

Land Payments

$0.30

$5

All-in Sustaining Costs (“AISC”)

$59.13

$986

Note: Total Cash Costs and AISC are non-GAAP measures and include royalties payable.

Project Royalties

The PEA considers two federal government royalties:

Underground Royalty: 3.0% of net smelter return of the mineral product.

Open Pit Royalty: 8.0% of net smelter return of the mineral product.

The production profile results in a blended royalty rate of 6.5%.

Capital Cost Estimates

The initial capital cost (“capex“) is estimated to be $936 million after accounting for $29 million in pre-production credits. A 12% contingency totaling $100 million is included in the estimate. Underground-related capex is captured in sustaining capex, with ramp development to initiate in Year 1 of operations.

The total construction period, including the early works program, is forecast to be 28 months.

Table 8: Capital Cost Summary

Initial CAPEX

USD M

100 – Infrastructure

$71

200 – Power & Electrical

$118

300 – Water Management

$16

400 – Surface Operations

$46

500 – Mining

$129

600 – Process Plant

$190

700 – Construction Indirects

$107

800 – General Services / Owner’s Costs

$111

900 – Pre-Production, Start-up & Commissioning

$76

990 – Contingency (12%)

$100

Capital Costs

$965

Less: Pre-Prod. Credit net of TC/RC & Royalties

($29)

Total Capital Costs

$936

The sustaining capex is estimated to be $574 million, including $37 million of closure and rehabilitation costs, split between open pit and underground operations. Open pit sustaining capex is earmarked for additional equipment, replacement units, and major repairs. Other sustaining capex captures tailings storage facility raises, process plant, power plant expansion, and G&A.

Table 9: Sustaining Cost Summary

Sustaining Capex

USD M

USD/oz

Open Pit

$216

$48

Underground (Initial capex)

$124

$28

Underground

$133

$30

Other

$64

$14

Sustaining Capex

$537

$120

Closure & Rehabilitation

$37

$8

Total Sustaining Capex

$574

$128

UG sustaining capex totals $257 million and includes lateral and vertical development of the mine, mobile equipment, fixed equipment, construction, and pre-production. The initial 2 years of construction and development total $124 million (48% of total UG sustaining capex). The table below sets out more details on the underground portion of the sustaining capex.

Table 10: Underground Sustaining Cost Summary

Underground Sustaining Capex

USD M

Lateral Development

$97

Mobile Equipment UG

$63

Construction UG

$29

Pre-Production UG

$26

Vertical Development

$13

Fixed Equipment UG

$12

Mobile Equipment UG Rebuild

$11

Other Equipment UG

$5

Total Underground Sustaining Capex

$257

Project Timetable and Next Steps

Corporate Timetable and Next Steps

Upcoming key milestones include:

Q4-2024: Oko Exploration results

Q4-2024: Tocantinzinho Gold Mine (“TZ“) exploration results

Q1-2025: TZ nameplate capacity

Q1-2025: Oko Feasibility Study

H1-2025: Oko Early Works and Construction Decision

H2-2027: Oko Commissioning

H1-2028: Oko Commercial Production

Preliminary Economic Assessment Study 3D VRIFY Presentation

To view a 3D VRIFY presentation of the Study please click on the following link: https://vrify.com/decks/16400 or visit the Corporation’s website at www.gmin.gold.

Updated corporate presentation is available at: https://vrify.com/decks/14338.

Technical Report Preparation and Qualified Persons

The Study has an effective date of September 4, 2024 and was issued on September 9, 2024. It was authored by independent Qualified Persons and is in accordance with National Instrument 43-101 – Standards of Disclosure for Mineral Projects.

GMS was responsible for the overall report and PEA coordination, property description and location, accessibility, history, mineral processing and metallurgical testing, mineral resource estimation, mining methods, recovery methods, project infrastructures, operating costs, capex, economic analysis and project execution plan. For readers to fully understand the information in this news release, they should read the technical report in its entirety, including all qualifications, assumptions, exclusions and risks. The technical report is intended to be read as a whole and sections should not be read or relied upon out of context.

The Qualified Persons (“QPs“) are Paul Murphy, P. Eng. having overall responsibility for the Report including capital and operating costs. Neil Lincoln, P. Eng. having responsibility for metallurgy, recovery methods and process plant operating costs. Christian Beaulieu, MSc, PGeo, of Minéralis Consulting Services is responsible for property description, geology, drilling, sampling and the mineral resource estimate. Alexandre Burelle, P. Eng. is responsible for the mining method and capital and operating costs related to the mine and the economic analysis. Derek Chubb, P. Eng., of ERM Consultants Canada Ltd., is responsible for the environment and permitting aspects.

The technical content of this press release has been reviewed and approved by the QPs who were involved with preparation of the Study. In addition, Louis-Pierre Gignac, President & Chief Executive Officer of GMIN, a QP as defined in NI 43-101, has reviewed the Study on behalf of the Corporation and has approved the technical disclosure contained in this news release. The PEA is summarized into a technical report that is filed on the Corporation’s website at www.gmin.gold and on SEDAR+ at www.sedar.com in accordance with NI 43-101.

About G Mining Ventures Corp.

G Mining Ventures Corp. (TSX: GMIN) (OTCQX: GMINF) is a mining company engaged in the acquisition, exploration and development of precious metal projects to capitalize on the value uplift from successful mine development. GMIN is well-positioned to grow into the next mid-tier precious metals producer by leveraging strong access to capital and proven development expertise. GMIN is currently anchored by the Tocantinzinho Gold Mine in Brazil and Oko West Project in Guyana, both mining friendly and prospective jurisdictions.

Additional Information

For further information on GMIN, please visit the website at www.gmin.gold.

Cautionary Statement on Forward-Looking Information

All statements, other than statements of historical fact, contained in this press release constitute “forward-looking information” and “forward-looking statements” within the meaning of certain securities laws and are based on expectations and projections as of the date of this press release. Forward-looking statements contained in this press release include, without limitation, those related to the PEA results (as such results are set out in the various charts, figures, graphs, schedules and tables featured hereinabove, and are commented in the text of this press release), such as the Project’s production profile, LOM, construction and payback periods, NPV, IRR (direct/indirect, before/after tax), startup capital costs, contingency, operating costs, AISC, sustaining capital costs, free cash flows, M&I resources, OP and UG mining phases, mill feed, milling process, recovery and output (for hard rock as well as saprolite), power supply arrangements and power consumption (and potentially available alternatives), and closure costs. Forward-looking statements also include, without limitation, those related to (i) the job creation, (ii) the targeted ESIA submission (iii) the EPA authorization and permitting process in general, (iv) the quoted comments of GMIN’s President & CEO and, more generally, the contents of the above sections entitled “Project Timetable and Next Steps”, “Corporate Timetable and Next Steps” and “About G Mining Ventures Corp.”.

Forward-looking statements are based on expectations, estimates and projections as of the time of this press release. Forward-looking statements are necessarily based upon a number of estimates and assumptions that, while considered reasonable by the Corporation as of the time of such statements, are inherently subject to significant business, economic and competitive uncertainties and contingencies. These estimates and assumptions may prove to be incorrect. Such assumptions include, without limitation, those underlying the items listed in the above section entitled “About G Mining Ventures Corp.” and:

long-term consensus gold price at $1,950 per ounce;

the USD:CAD foreign exchange rate;

low inflation environment and Guyana’s developing economy;

the various tax assumptions;

the capital cost estimates being supported by budgetary quotes; and

the Project’s permitting expectations, notably obtaining the EPA authorization.

Many of these uncertainties and contingencies can directly or indirectly affect, and could cause, actual results to differ materially from those expressed or implied in any forward-looking statements. There can be no assurance that, notably but without limitation:

all permits necessary to build and bring Oko into commercial production will be obtained or, as applicable, reinstated;

the price of gold environment and the inflationary context will remain conducive to bringing Oko into commercial production;

the business conditions in Guyana will remain favorable for developing mining projects such as Oko; and

the Corporation will bring Oko into commercial production and that it will acquire any other significant gold assets.

In addition, there can be no assurance that, notably but without limitation, (i) the Corporation will use TZ as the flagship asset to grow GMIN into the next mid-tier precious metals producer and (ii) Brazil and Guyana will remain mining friendly and prospective jurisdictions, as future events could differ materially from what is currently anticipated by the Corporation.

By their very nature, forward-looking statements involve inherent risks and uncertainties, both general and specific, and risks exist that estimates, forecasts, projections and other forward-looking statements will not be achieved or that assumptions do not reflect future experience. Forward-looking statements are provided for the purpose of providing information about management’s expectations and plans relating to the future. Readers are cautioned not to place undue reliance on these forward-looking statements as a number of important risk factors and future events could cause the actual outcomes to differ materially from the beliefs, plans, objectives, expectations, anticipations, estimates, assumptions and intentions expressed in such forward-looking statements. All of the forward-looking statements made in this press release are qualified by these cautionary statements and those made in the Corporation’s other filings with the securities regulators of Canada including, but not limited to, the cautionary statements made in the relevant sections of the Corporation’s (i) Annual Information Form dated March 27, 2024, for the financial year ended December 31, 2023, and (ii) Management Discussion & Analysis. The Corporation cautions that the foregoing list of factors that may affect future results is not exhaustive, and new, unforeseeable risks may arise from time to time. The Corporation disclaims any intention or obligation to update or revise any forward-looking statements or to explain any material difference between subsequent actual events and such forward-looking statements, except to the extent required by applicable law.

SOURCE G Mining Ventures Corp

Jessie Liu-Ernsting, Vice President, Investor Relations and Communications, 647.728.4176, [email protected]

Source link : http://www.bing.com/news/apiclick.aspx?ref=FexRss&aid=&tid=66e2d9d1dd014c11be80a91f6fd02d8b&url=https%3A%2F%2Fwww.newswire.ca%2Fnews-releases%2Fg-mining-ventures-delivers-pea-for-high-grade-oko-west-gold-project-in-guyana-810362650.html&c=15000679825798892328&mkt=en-us

Author :

Publish date : 2024-09-09 00:00:00

Copyright for syndicated content belongs to the linked Source.

{kind=link}